Open banking is revolutionizing the financial landscape, presenting both exciting opportunities and significant challenges. It promises to empower consumers with greater control over their financial data, fostering innovation and competition in the financial services industry. Open banking initiatives are driving the development of new financial products and services, potentially leading to more personalized and cost-effective solutions for individuals and businesses. Understanding the implications of this transformative trend is crucial for both consumers and financial institutions. This article will delve into the dynamic landscape of open banking, exploring the opportunities it unlocks and the challenges that must be addressed to ensure its responsible and beneficial implementation.

The core principle of open banking is the secure sharing of consumer financial data with third-party providers through Application Programming Interfaces (APIs). This allows authorized third parties to access a consumer’s banking information, such as transaction history and account balances, to develop innovative financial products and services. While the potential benefits of open banking are numerous, including increased competition, enhanced customer experiences, and greater financial inclusion, several challenges related to data security, privacy, and regulatory compliance need careful consideration. This article examines the multifaceted aspects of open banking, analyzing the opportunities for growth and innovation alongside the challenges that need to be overcome for its widespread adoption and long-term success.

Understanding Open Banking

Open Banking refers to a banking practice that provides third-party financial service providers open access to consumer banking, transaction, and other financial data from banks and non-bank financial institutions through the use of application programming interfaces (APIs).

Consent plays a vital role. Customers give explicit permission for their data to be shared. This allows third-party developers to build applications and services that can offer personalized financial management tools, create innovative payment methods, and facilitate easier access to credit and other financial products.

Data security is paramount. Open Banking relies heavily on secure APIs and robust authentication measures to protect sensitive financial information from unauthorized access and misuse.

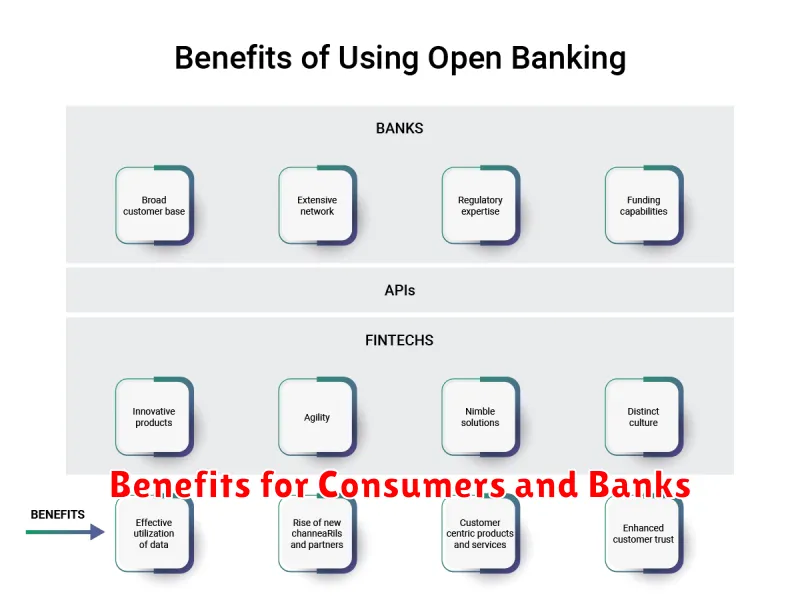

Benefits for Consumers and Banks

Open banking offers numerous advantages for both consumers and banks. For consumers, it fosters increased competition among financial providers, leading to better products and services. Personalized financial management becomes more readily available through aggregated financial data and tailored advice. Consumers also gain greater control over their financial data and how it is utilized.

Banks benefit from open banking through the creation of new revenue streams. By leveraging APIs, banks can develop innovative financial products and services, attracting new customers and enhancing existing relationships. Improved efficiency is another key benefit, as open banking streamlines processes such as loan applications and KYC procedures.

Risks Associated with Open Banking

While open banking presents numerous opportunities, it also introduces several risks that must be carefully addressed. Data security and privacy are paramount concerns. The increased flow of sensitive financial information between different parties raises the potential for data breaches and misuse.

Fraud and scams are another significant risk. Criminals may exploit vulnerabilities in the system to gain unauthorized access to accounts. Third-party provider risk is also a concern. The reliance on external providers introduces dependencies and potential vulnerabilities if these providers lack adequate security measures or experience financial difficulties.

Finally, consumer protection is crucial. Clear regulations and mechanisms are necessary to ensure consumers understand the risks, have control over their data, and have recourse in case of issues.

Regulatory Landscape

The regulatory landscape surrounding open banking is evolving rapidly and varies significantly across jurisdictions. Standardization and interoperability are key goals for regulators aiming to foster competition and innovation.

Many regions are adopting frameworks based on principles of data privacy, consumer consent, and secure data sharing. These regulations often specify technical standards, security protocols, and licensing requirements for third-party providers (TPPs) accessing customer data.

Enforcement and oversight also play a crucial role in ensuring the responsible development of open banking. Regulators monitor compliance and address potential risks related to data breaches, anti-competitive practices, and consumer protection.

Future Prospects of Open Banking

Open banking holds significant promise for the future of finance. Increased competition and innovation are expected as new financial products and services emerge. This will likely lead to more personalized and efficient financial management for consumers.

Expansion beyond traditional banking services is also anticipated. Integration with other sectors, such as healthcare and telecommunications, could unlock further benefits. Moreover, open banking could play a crucial role in driving financial inclusion by providing access to financial services for underserved populations.

However, realizing the full potential of open banking hinges on addressing key challenges, such as data security and consumer privacy. Establishing robust regulatory frameworks and promoting interoperability will be vital for fostering trust and ensuring sustainable growth.

{kind=link}